While countries like Panama and El Salvador open more doors for crypto, China chose the repression route.

The People’s Bank of China(PBoC)— China's central bank— announced that it is banning all crypto-related activities nationwide for the second time in four years. The statement also warns that all nationals working for overseas cryptocurrency exchanges will be investigated. Crypto production (mining) services like Spark Pool, which makes up 25% of Ethereum's production pool, have shut down due to the ban.

Chinese regulators have had it in for virtual currencies for a while: China banned crypto exchanges five years ago, and over the past year, various parts of the country banned mining and crypto trading. In May, PBoC banned domestic crypto exchanges in a bid to obliterate crypto trading, so Chinese traders switched foreign platforms.

What's China up to? PBoC is currently running a pilot on their digital currency, Chinese yuan (e-CNY). Speculators believe this could be the reason the authorities are being particularly tough about this new ban cycle.

Not everyone is China: In contrast, institutions like The United Arab Emirates' Securities and Commodities Authority are embracing crypto assets. So are financial institutions and some of the highest-valued companies around the world.

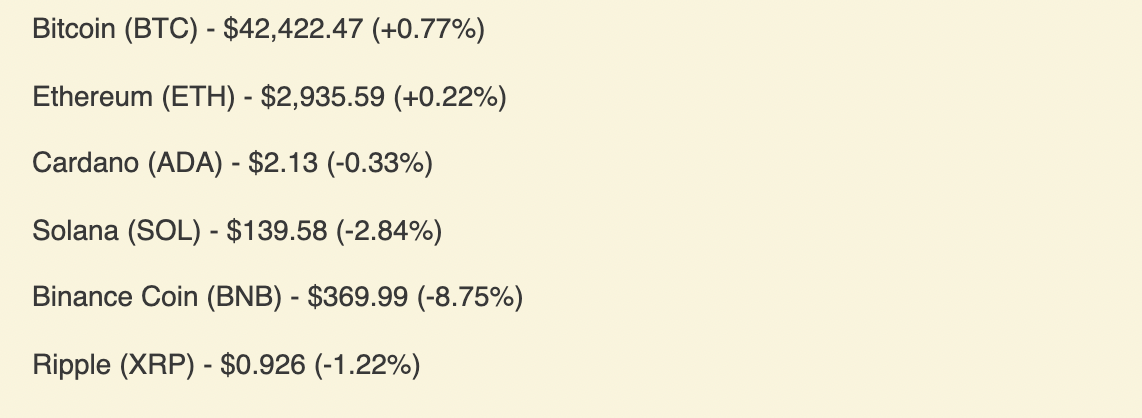

Market reaction: The value of the crypto market dropped by about 5% as soon as this ban was announced, but this is expected because major news (good or bad) very often triggers a market reactionary effect. The good thing is that the market always readjust.

Botton line: This isn't the first time. In 2017, China's ban on crypto triggered a value drop that lasted a few weeks. But, as Decrypt Editor Dan Robert pointed out during El Salvador's bitcoin-as-currency launch, a country's relationship to crypto might not mean much in the long run. A better indicator of crypto's place in finance is that more traditional investors are getting into it.